Tribal Politics, Power Struggles, and the Cost to Our Community

By Joe Morey

Today, I want to share what has truly transpired at Big Fish Golf Course,

and why our LCO Tribal Chairman set out on a mission to destroy me. This isn't

just a personal dispute—it's about tribal politics gone wrong, with no regard

for the future of our beautiful golf course. The course, and everything we

worked so hard to build, was sacrificed for one man’s agenda: to silence me in

fear that I could expose a land deal that benefited him personally, at great

cost to the Tribe.

The land in question lies at the corner of Hwy B & K with C2,

Sevenwinds and Dollar General. I’ll explain more about that deal later.

The Crisis at Big Fish and My

Appointment as Interim GM

On December 7, as Vice Chairman of the Big Fish Golf Board, I faced a

critical moment. The course was running out of money. We had two options: shut

down for the winter or act fast to turn things around. The board at that time

consisted of Chris Rusk (Chairman), Cameron Quaderer, Michelle Beaudin, Tweed

Shuman, and myself.

That day, the board agreed to appoint me as interim general manager. I

brought 20 years of restaurant and bar management experience to the table, and

with winter approaching, the focus needed to shift toward food and beverage

operations. We had 12 active employees on payroll while all seasonal staff had

already been laid off. One major issue was that seasonal employees had been

kept on too long, draining the funds made during the 2024 season.

Chris Rusk had initially proposed a different candidate—someone

handpicked by him—but neither the board nor the Tribal Council supported that

choice. From that moment on, Chris began working to undermine my leadership,

aided by his uncle, Chairman Louis Taylor.

The Conflict of Dual Roles and

Targeted Scrutiny

Despite the precedent of others on the reservation holding multiple

high-paying roles (one with a salary at $200,000 annually), Louis, Tweed, and

David Bisonette decided I couldn’t hold two jobs—even though I offered to

continue doing graphic design and communications work for half the pay.

I proposed this compromise because a newly hired public relations person

could take on the writing responsibilities, allowing me to focus on Big Fish.

But they wouldn’t budge. It became clear: Louis saw me as a threat and was

determined to remove me, using his nephew Chris Rusk to do the dirty work.

Turning Big Fish Around

From day one, it was obvious how bad things had become. There was no

clear management, department heads weren’t communicating, and some weren’t even

speaking to each other. I held a meeting and shared my vision—we were starting

fresh, and everyone needed to work together.

In the months that followed, we launched a major marketing campaign for

the restaurant and a membership sale, generating over $108,000 in 30 days. I

also uncovered $65,000 in unpaid debt from the previous season—utilities,

vendor payments, and pro shop inventory. We paid off that debt and invested

$25,000 into facility improvements. We added a PA system, installed big screens

with full connectivity, hung vintage golf photos, and improved the POS system.

These upgrades transformed our event center into a desirable space for

community events.

Soon, we were booking private events and doing less of our own, and daily

food sales rose from nearly nothing to over $1,000 per day. Memberships also

surged—from a decline in 2024 (27,000 rounds in 2023 down to 21,000 and a loss

of over 100 members)—to nearly 300 memberships by last week. We set out with a

goal to surpass 30,000 rounds this season.

Undermined by Politics Despite Success

Despite our success, none of it mattered to the golf board or Tribal

Chairman. They were focused solely on silencing me and stopping the exposure of

the land deal. Golf board members included Rusk, Cameron Quaderer, Don

Quaderer, Tweed Shuman, and Michelle Beaudin—though Michelle was often excluded

from meeting notices and financial disclosures.

Financial Smokescreens and False

Claims

Throughout my four-month tenure, I never received a Profit & Loss

statement from our assigned enterprise accounting bookkeeper, Melissa Kagigebi.

In a recent email thread with the Tribal Council, golf board, and enterprise

accounting, Melissa falsely claimed I had overspent and left only $6,000 in the

account. This misinformation was repeated by board members to staff after I was

escorted out by eight county deputies and conservation wardens.

A concerning and misleading narrative has been circulated regarding my

management of Big Fish Golf operations—one that misrepresents financial

realities and appears to be driven by a personal agenda. Among the most

damaging claims was a payables list sent out by Melissa Kagigebi, designed to

make it appear as though I had accumulated over two hundred thousand dollars in

debt. However, this portrayal ignored key facts.

First, the majority of those payables were tied to net 60 terms on

merchandise ordered by the pro shop manager—standard practice for golf retail

operations. Additionally, the list included $60,000 in previous payroll debt,

specifically Christmas bonuses authorized by the prior manager. These bonuses

were never approved by the golf board. The funds were temporarily covered by

the tribal office payroll, with the understanding that Big Fish would repay the

amount. Presenting this as debt incurred under my leadership is both misleading

and unfair.

Following these claims, I immediately went to the bank to obtain a

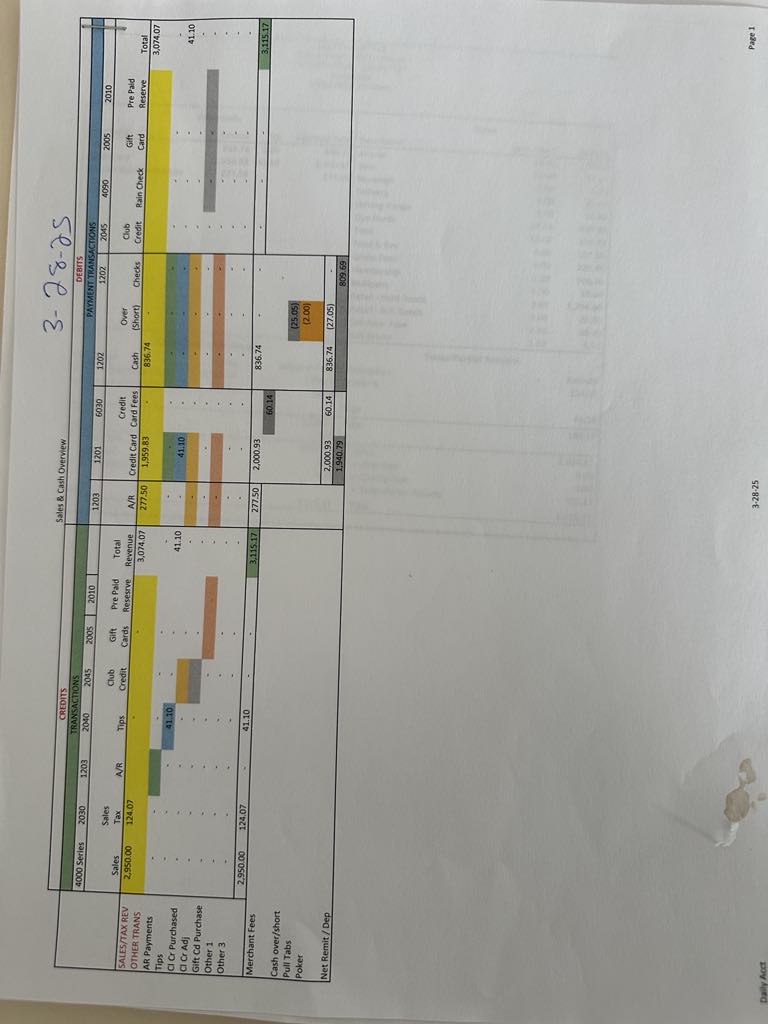

current statement and address the false report that only $6,000 remained in the

account. The actual balance was $42,000. When challenged, Melissa shifted her

explanation, stating there were pending checks yet to clear. I asked for a

detailed list of those outstanding checks. She delayed, citing reconciliation

tasks, and finally sent a list a day later. That list, however, included checks

that had already cleared—a fact pointed out in the email chain by Michelle

Beaudin. After correcting for cleared checks, the actual amount pending was

just $15,000, leaving $27,000 in the account—a far cry from the initial claim

of $6,000. There was a $10,000 check for Bartingale Mechanical she had on the list,

but that check had never been signed nor approved for payment so it was

misleading on her part to include that on the payables list.

Weekly Meetings and Agenda-Driven Reporting

This was not an isolated incident. Over a period of a few months leading

up to the board’s move to terminate my position, I was continuously undermined

by misinformation fed to the golf board, aimed at painting a picture of

financial mismanagement. Chris Rusk, during this time, began calling weekly

golf board meetings—an unprecedented shift, considering that during my five

years on the board, meetings were held monthly at most. Despite being expected

to defend my role, I was denied access to the necessary financials—such as

profit and loss statements—that would have allowed me to prepare a proper

report. I would arrive at meetings to find that Melissa had already presented

her narrative, leaving me on the defensive without context or documentation.

Historically, the general manager would present their report to the

board, and the bookkeeper would be called in only when specific questions

arose. This changed while I was interim GM, which appeared increasingly aligned

with a personal effort to discredit me. Eventually, I refused to participate in

this dysfunction and instead shared the truth with tribal council members I

trusted, including Michelle Beaudin—who also serves as secretary-treasurer of

the golf board yet was excluded from meeting notices and discussions—as well as

Bill Trepanier, Don Carley, and Little Guy.

Conflicts of Interest and Mismanagement

It became evident that a small group, closely tied to Chris Rusk, was

orchestrating efforts against me. This group included Melissa and others with

similar agendas. Following the vote to terminate me, the board appointed a new

general manager—John Quaderer, a Big Fish mechanic and father of board member

Cameron Quaderer. Cameron’s involvement in the vote and subsequent appointment

process raises ethical concerns and should have disqualified him from

participating.

Moreover, I pointed out immediately that John Quaderer is a St. Croix

tribal member, which, as of now, has delayed his assumption of the general

manager role.

Over the past week, I’ve taken a step back to observe the results of

these actions. Unfortunately, the consequences have been swift and damaging.

Promotions have ceased, marketing efforts are nonexistent, recipes are already

being altered, and money is unaccounted for. Chris Rusk and his associates are

now golfing in large groups, using up to five carts per group—an allowance not

extended to regular golfers but seemingly acceptable due to his status as board

chairman. Meanwhile, current staff admit they are in over their heads and

struggling to manage the operation.

The environment is rapidly regressing to the disorganized and

conflict-ridden state it was in as of December 7. Communication among staff has

broken down. It’s heartbreaking to witness the dismantling of the progress we

made in just four months—progress undone by ego, hidden agendas, and political

gamesmanship at the expense of the operation’s future.

The Land Deal and Tribal Chairman

Misconduct

Now to the land deal. A formal complaint was filed with the LCO Tribal

Court by Adam DeNasha, a tribal member and aspiring attorney attending UW-La

Crosse. That complaint is printed in its entirety just below. He submitted it

first to the Tribal Governing Board, but they suspended the Tribal Code of

Conduct, rendering his complaint moot at the time.

Then, on Monday, April 7, Chairman Louis Taylor, along with Tweed Shuman

and David Bisonette, introduced an amended Code of Conduct that would grant

Tribal Governing Board members immunity for any misconduct while in

office—arguing that they should be sovereign just as the tribal governing board

is as a whole. The rest of the TGB opposed it, and the proposal was tabled—for

now.

They were expected to attempt passing it again at Monday’s meeting

yesterday.

The land deal below involves Chairman Louis Taylor selling the acreage across from the casino to the Tribe for $168,000 (valued at $43,000) after purchasing it from St. Croix Tribe for $20,000. The purchase amount from St. Croix was confirmed by sources at their Tribe.

Final Notes

Following this complaint printed in its entirety are documents supporting

the misconduct complaint, my projections report for Big Fish’s future, and all

relevant financial documentation.

CODE OF CONDUCT COMPLAINT/GIREVANCE

LAC COURTE OREILLES TRIBAL GOVERNING BOARD

CODE OF CONDUCT COMPLAINT/GRIEVANCE

I. INTRODUCTION

I, ADAM DENASHA, the Complainant, file this complaint

pursuant to MCC. I. I I .0 IO in good faith, alleging that the following

Elected Official, LOUIS D. TAYLOR, violated multiple Tribal Laws. The

Complainant is a tribal member of LCO and is exercising his constitutional

right to petition the TGB for redress of grievances. The grievances are

multiple violations of the Tribal Government Code of Conduct,§ MCC.l, and

violation of the Special Meetings Notice Requirement under§ MCC.2.5.020. The

Tribal Code of Conduct was established because the "citizens of the Tribe

are entitled to have complete confidence in the loyalty and integrity of their

Elected Officials. To that end this ordinance establishes clear standards of

ethical conduct and behavior of the Elected Officials to the Tribal Governing

Board. This ordinance seeks to require accountability to the citizens of the

Tribe by the Tribal Governing Board in exercising the authority vested with

them"(§ MCC.1.1.020). This petition is filed due to the loss of confidence

in the integrity of LOUIS D. TAYLOR. The redress of these grievances is

accountability and corrective actions to regain the confidence in the integrity

of the Tribal Governing Board, along with a report to the public on these

actions.

II. PARTIES'

INFORMATION

Complainant Name: Adam

DeNasha

Elected Official:

LouJs D. Taylor, Chairman

Ill. STATEMENT OF

FACTUAL BACKGROUND

Resolution No. 2023-108 "Temporary Suspension of MCC. l

Tribal Government Code of Conduct for Revision" was adopted on August 21,

2023. This Resolution suspended the Tribal Government Code of Conduct for a

total of" 180 days for revision, additions, and updates". The 180-day

suspension has since expired.

1. The Chairman of LCO, Louis D. Taylor,

has multiple connections to the St. Croix Tribe, including the period of

2014-2018.

2. In

December 2013, the St. Croix Tribe entered into an employment relationship with

Jeffrey S. Taylor. His position was the Chair of the St. Croix Gaming

Commissioner (see doc. A, pg 9, #54).

3. In July

2015, the St. Croix Tribe entered into an employment relationship with Kate

Wolfe Taylor. She was the Administrative Assistant for the Gaming Commission.

4. In

September 2014, Lewis Taylor was a member of the St. Croix Tribal Council.

5. Lewis

Taylor was one of eleven individuals involved in embezzlement from the St.

Croix Tribe's Casino from 2014 to 2017.

6. Jeffrey S.

Taylor was one of eleven individuals involved in embezzlement from the St.

Croix Tribe's Casino from 2015 to 2017.

7. Jeffrey S.

Taylor was alleged to have received improper disbursements totaling $55,481.37.

(see doc. A, pg. 9, #58).

8. Jeffrey S.

Taylor is an enrolled member of the St. Croix Tribe. (see doc. A, pg. 2, #7).

9. Kate Wolfe

Taylor was one of eleven individuals involved in embezzlement from the St. Croix

Tribe's Casino from 2015 to 2017.

10. Kate Wolfe

Taylor was alleged to have received improper disbursements totaling $30,590.

11. Kate Wolfe

Taylor is a non-Indian.

12. The NIGC

levied a 5.5 million dollar fine against the St. Croix Tribe in May 2019, which

included a "$1 million fine assessed for payments to Jeff Taylor and Kate

Wolfe Taylor of the Tribal Gaming Commission ... " as "[t]hese

individuals were responsible for protecting the tribal assets from abuse"

(see doc. A, pg. 9-10, #59).

13. Kate Wolfe

Taylor is married to Bruce Taylor.

14. Bruce Taylor

is the brother of the Chairman of LCO, Louis D. Taylor.

15. Jeffs.

Taylor is the son of the Chairman of LCO, Louis D. Taylor.

16. On September

15, 2014, Louis P. Taylor acquired a parcel of land from the St. Croix Chippewa

Indians of Wisconsin for an unknown amount. (see doc. B)

17. The Parcel

Identification Number, or "PIN", was: 010-841-28-3202 (hereinafter

"3202") with a legal description of"The NW¼ of the SW¼ of

Section 28, Township 21 North, Range 8 West, Town of Hayward, Sawyer County,

Wisconsin, EXCEPT that part lying North of the Town Road" (see doc. B).

1. From

2007-2017, the above parcel was listed as 18.5 acres.(see doc. C & D)

n. In

2018-2021, the above parcel was listed as 21.5 acres with no change to the

Legal Description. (see doc. E & F)

18. Lewis Taylor

signed the Warranty Deed on behalf of St. Croix Chippewa Indians of Wisconsin

as "Tribal Chairman" transferring ownership of parcel 3202 to Louis

P. Taylor. (see doc. B)

19. Louis P.

Taylor is an enrolled member of the St. Croix Tribe.

20. Louis P.

Taylor is the son of the Chairman of LCO, Louis D. Taylor.

21. In September

2017, the NIGC began an investigation of St. Croix's use of gaming revenue.

(see doc. A, pg. 9, #56).

22. In March

2018, just six months after St. Croix started being investigated, Louis P.

Taylor signed the land over to his father, the Chairman, Louis D. Taylor. The

sale price, if any, is unknown. (see doc. G)

23. On November 15, 2021, the Chairman, Louis

D. Taylor, sold 19.45 acres out of the 21.5 acres of the land to the Lac Courte

Oreilles Band of Lake Superior Chippewa Indians of Wisconsin. (see doc. H)

24. Louis D.

Taylor did not engage in negotiations, Louis P. Taylor did negotiations for the

sale of parcel 3202.

25. The legal

description for the land acquired from the Chairman, Louis D. Taylor, by LCO is

as follows:

"Lot 1 as recorded in Volume 37 of Certified Survey

Maps, page 220, Survey No. 8597 as Document No. 435876, located in the Town of

Hayward, Sawyer County, Wisconsin, being a part of NW¼ SW¼, Section 28,

Township 41 North, Range 8 West." (see doc. H)

26. Parcel 3202

has two child parcels, the 19.45-acre lot with PIN "0 10-841-28-3206"

(hereinafter "3206") owned by LCO and the two-acre lot with PIN

"0 10-841-28-3207" owned by Louis D. Taylor. (see Doc. K)

27. The 2022 Tax

Record shows that this land has a "Total Value" of $31,400, with a

"Total Estimated Fair Market" (hereinafter "EFM") of

$40,600. (see doc. I)

28. The Warranty

Deed (#435952) shows that the Transfer fee was $504.00. (see doc. H)

29. According to

Wis. Stat.§ 77.22(1), "There is imposed on the grantor of real estate a

real estate transfer fee at the rate of 30 cents for each $100 of value or

fraction thereof on every conveyance ... ", meaning the transfer fee is

0.3%.

30. Calculations

show that the Chairman, Louis D. Taylor, sold this land to LCO for $168,000.00.31.

No agreement for this land was ever made public, and the complainant, Adam

DeNasha, was unable to review any record of this agreement or the Warranty

Deed, as the complainant bought a copy of the warranty deed online.

32. The sale

price of the parcel sold by Louis D. Taylor, as determined by Realty, was based

on the price LCO paid for the adjacent 36.610-acre parcel, PIN

"010-841-28-3303" (hereinafter "3303"), which was roughly

$250,000. (see doc. J for acreage, doc. K for PIN)

33. In 2007,

parcel 3303 had an EFM of $254,300. (see doc. J)

34. In 2007,

parcel 3202 had an EFM of $52,800. (see doc. C)

35. The EFM

considers surrounding property prices in its calculations, which is shown in

the 2014 & 2015 Tax Records of each parcel:

1. 2014 EFM

of:

a. 3202 -

$46,000 (see doc. L)

b. 3303 -

$221,800 (see doc. M)

11. 2015 EFM of:

a. 3202 -

$30,600 (see doc. N)

b. 3303 - $0

(Parcel was placed in trust) (see doc. 0)

36. LCO paid the

close to the EFM for parcel 3303 in 2006.

37. LCO paid

more than four times the EFM for parcel 3202 in 2021.

IV. ALLEGED

MISCONDUCT AND LAWS VIOLATED

In addition to Tribal Laws, each alleged misconduct violates

the traditional and cultural values of Wisdom, Love, Respect, Bravery, Honesty,

Humility, and/or Truth. Per§ MCC. l.3.070(b)(5), "Elected Officials will

adhere to the principles of this ordinance by... Tak[ing] alleged violations

and suspected violations seriously, as they could delay, compromise, or

otherwise impair the services the Tribe provides". The Complainant alleges

that the following acts, numbered 38-42, violate the subsequent laws:

38. Louis D. Taylor obtained land that was

previously owned by the St. Croix Tribe, and sold it to the LCO Tribe, more

than four times its EFM value. This violates the following:

1. § MCC. I

.3.020 (a) "Elected Officials shall represent the interests of all members

of the Tribe and not serve special interests inside or outside of the

Tribe."

11. § MCC.1.3.020 (b)(3) "To fully represent the

interests of the Tribe, Elected Officials shall... Refuse any offer that has

the appearance of being an illegal or inappropriate offer, solicitation,

payment, or remuneration".

m. § MCC. l.3.060(b)(3) "To maintain confidence in the

Tribal government, such officials shall ... " "Conduct business

dealings in a manner such that the Tribe shall be the beneficiary of such

dealings".

1v. § MCC.1.4.0IO(a) "No Elected Official shall use, or

attempt to use, any official or apparent authority of their office or duties

which places, or could reasonably be perceived as placing their private

economic gain or that of any special business interests with which they are

associated, before those of the Tribal membership, whose paramount interests

their office or employment is intended to serve".

v. § MCC.1.4.010 (b)(I) "It is the intent of this

section that the Elected Officials of the Tribe avoid any action, whether or

not specifically prohibited by the provisions of this ordinance as set out

herein, which could result in, or create the appearance of... Using public

office for private gain" (emphasis added).

v1. § MCC.1.4.010 (b)(5) "It is the intent of this

section that the Elected Officials of the Tribe avoid any action, whether or

not specifically prohibited by the provisions of this ordinance as set out

herein, which could result in, or create the appearance of... Making a

government or management decision outside official channels" (emphasis

added).

v11. § MCC.1.4.010 (b)(6) "It is the intent of this

section that the Elected Officials ofthe Tribe avoid any action, whether or not

specifically prohibited by the provisions of this ordinance as set out herein,

which could result in, or create the appearance of... Adversely affecting the

confidence of the Tribal members in the integrity of the government and

administration of the Tribe" (emphasis added).

39. How this land was obtained by the Chairman's son, Louis

P. Taylor, due to the illegal activity going on at the time Louis P. Taylor

obtained the land, appears to be unethical, if not illegal, as his brother

Jeffrey S. Taylor was also involved in the embezzlement of Tribal funds. Louis

D. Taylor is connected to the former Chairman of St. Croix, Lewis Taylor, and

without a resolution from the St. Croix tribe, this appears to be, not only

unethical but illegal. This violates the following:

1. § MCC.1.3.020 (b)(l) "To fully represent the

interests of the Tribe, Elected Officials shall... Not engage in any business

activity that appears to be unethical or illegal".

11. §

MCC.1.4.0 IO (b)( l) "It is the intent of this section that the Elected

Officials of the Tribe avoid any action, whether or not specifically prohibited

by the provisions of this ordinance as set out herein, which could result in,

or create the appearance

of... Using public office for private gain" (emphasis

added).

40. The

Complainant asked to see the deed, but the Realty employee did not know if I

was allowed, so did not allow me to see it. The Complainant was denied direct

access to the amount LCO Tribe paid for the land. The Complainant had to review

Wisconsin laws and buy a copy of the deed to figure out the Transfer fee and

calculate the price the Tribe paid.

Not allowing the land

purchase agreement to be viewed by the public is not dealing openly or honestly

with fellow Tribal members and violates the following:

1. LCO CONSTITUTION, ART. V § l. (j) "All expenditures

by the Governing Board shall be in accord with a previously approved budget,

and the amount so paid shall be a matter of public record at all times"

11. § MCC. l.3.060(b)(2) "To maintain confidence in the

Tribal government, such officials shall... " "Deal openly,

effectively, and honestly with fellow Tribal members, Elected Officials,

employees, contractors, government agencies and others".

m. § MCC.1.4.0 IO (b)(I) "It is the intent of this

section that the Elected Officials of the Tribe avoid any action, whether or

not specifically prohibited by the provisions of this ordinance as set out

herein, which could result in, or create the appearance of. .. Using public

office for private gain" (emphasis added).

1v. § MCC.l.4.010 (b)(6) "It is the intent of this

section that the Elected Officials of the Tribe avoid any action, whether or

not specifically prohibited by the provisions of this ordinance as set out

herein, which could result in, or create the appearance of... Adversely

affecting the confidence of the Tribal members in the integrity of the

government and administration of the Tribe" (emphasis added).

41. Due to the Chairman's position as a member of the TGB,

the Chairman knew or reasonably should have known, that the Tribe wanted to

acquire that parcel of land from St. Croix. The Chairman acquired it intending

to sell it to LCO Tribe at an excessively inflated price. This violates the

following:

1. § MCC.1.5.0IO(a)(9) "To avoid using governmental

positions to serve their own personal, financial, or business interests...

Elected Officials shall not engage in transactions that will provide them an

economic advantage due to information received through their public office or

employment, and such officials shall not acquire any property or other economic

interests when doing so that will substantially affect or influence the

performance of the official actions or duties".

11. § MCC. l.5.030(a)(3) "Except as otherwise provided

herein or by applicable rule or regulation adopted hereunder by the Tribe, or

by other applicable law, no Elected Official shall solicit or accept for

themselves or another, any gift, including economic opportunity, favor,

service, or loan (other than from a regular lending institution or Tribally

sponsored lending program on generally available terms) or any other benefit

from any person, organization or group which... Has any interest which, within

the past two years or in the foreseeable future, has been or will be directly

affected by an official action (or inaction) of such Elected Official or the

Election Official's office".

42. Louis D.

Taylor took ownership of this parcel six months after St. Croix came under

investigation to prevent the loss of the land. This allegation violates the

following:

1. § MCC. l .3.020 (a) "Elected Officials shall

represent the interests of all members of the Tribe and not serve special

interests inside or outside of the Tribe."

11. § MCC.1.3.020 (b)(1) "To fully represent the

interests of the Tribe, Elected Officials shall... Not engage in any business

activity that appears to be unethical or illegal" (emphasis added).

m. § MCC.1.3.020

(b)(3) "To fully represent the interests of the Tribe, Elected Officials

shall ... Refuse any offer that has the appearance of being an illegal or

inappropriate offer, solicitation, payment, or remuneration".

1v. § MCC.1.4.0 I 0(b)(6) "It is the intent of this

section that Elected Officials of the Tribe avoid any action, whether or not

specifically prohibited by the provisions of this ordinance as set out herein,

which could result in, or create the appearance of. .. Adversely affecting the

confidence of the Tribal members in the integrity of the government and

administration of the Tribe" (emphasis added).

Each of the aforementioned violations violates §

MCC.1.3.070(b)I) "Elected Officials will adhere to the principles of this

ordinance by... Becoming familiar with the provisions of this ordinance and the

policies and procedures applicable to Elected Officials".

V. RESOLUTION

2023-108, THE SUSPENSION OF§ MCC.l AND STATUTE OF LIMITATIONS

Regarding§ MCC.1.11.080 "Statute of Limitations",

it would not bar this claim in this instance. The Deed was signed to LCO Tribe

on November 15, 2021, which would've made the deadline to present the claim

November 15, 2023, however, Resolution No. 2023-108 was signed on August 21,

2023, suspending the Tribal Government Code of Conduct. That resolution being

signed statutorily prohibited claims from being presented and the time during

this prohibition does not toll the time for the statute of limitations but

rather extends it by the number of days of the statutory prohibition period.

The prohibition period started the day the Resolution was enacted (August 21,

2023) to the date that would have been the expiration date (November 15, 2023),

which is 86 days. Resolution 2023-108 expired on February 17, 2024, which

started the toll of 86 days, making the deadline May 19, 2024.

VI. REQUESTED

RELIEF

Remove Louis D. Taylor from the position of Chairman until

the investigation is complete and prohibit him from being the Vice Chairman as

well. He should be prohibited from being included in any official conversations

between the LCO Tribal Governing Board and St. Croix's Tribal Council.

No Tribal Law requires public disclosure of the

investigation, but to strengthen the complete confidence in the integrity and

loyalty of the Tribal Governing Board that Tribal Members are entitled to have,

a report of any findings of this claim should be made public. This benefits the

Tribe as a whole regardless of the findings. If the allegations are found to be

true, then the Tribal Governing Board should move forward with immediate

removal and any possible civil and/or criminal proceedings that may be applicable.

If allegations are found to be disproven, this would clear the name of Louis D.

Taylor and show the public that Louis D. Taylor maintained his integrity. This

is crucial considering his ties, directly or indirectly, to the embezzlement of

St. Croix's Tribal funds.

VII. CONCLUSION

The LCO CONSTITUTION, ART. VII states that"... no

member shall be denied freedom of conscience, speech, religion, association or

assembly, nor shall be denied the right to petition the Governing Board for the

redress of grievances against the Band" and per § MCC.1.11.0 I 0, the

complainant is exercising the Constitutional right to petition the Governing

Board redress of grievances to demand accountability for violations of the Code

of Conduct as Tribal members are ENTITLED to have complete confidence in the

integrity and loyalty of the Tribal Governing Board. By law, the TGB must take

the alleged allegations seriously. Any failure to take the allegations

seriously results in the violations of a tribal member's constitutional right

to petition the Tribal Governing Board for the redress of grievances. With the

right to grieve comes the right to redress, otherwise the right to grieve is

fruitless.

The Tribal Governing Board, sans Louis D. Taylor, needs to

discuss with the Tribal Attorneys the legality of the transactions and possible

outcomes. The Complainant suggests that the Tribal Governing Board, sans Lewis

D. Taylor, open discussions with the St. Croix Tribe and request the resolution

approving the transfer of the land to Louis P. Taylor, and the sale price of

the land to know there was a legitimate transaction. Due to Public Law 280,

along with the Tribe not having laws regarding fraudulent real estate

transfers, claims may go through the State Court.

Signed on this 23rd day of February 2024. AJ:Q

Adam DeNasha

Additional Documents Attached to Support Claims:

A. Complaint

for St. Croix v. Jeffrey Taylor, 20-CV-208, (St. Croix Tribal Court, 2020)

B. Warranty

Deed 392326. St. Croix Chippewa Indians of Wisconsin to Louis P. Taylor

C. Sawyer

County Tax Bill for 2007 for parcel 3202 owned by St. Croix

D. Sawyer

County Tax Bill for 2017 for parcel 3202 owned by Louis P. Taylor

E. Sawyer

County Tax Bill for 2018 for parcel 3202 owned by Louis D. Taylor

F. Sawyer

County Tax Bill for 2021 for parcel 3202 owned by Louis D. Taylor

G. Warranty

Deed #411640. Louis P. Taylor to Louis D. Taylor

H. Warranty

Deed #435952. Louis D. Taylor to LCO

I. Sawyer

County Tax Record for 2022 for parcel 3206 owned by LCO

J. Sawyer

County Tax Bill for 2007 for parcel 3303 owned by LCO

K. Sawyer

County parcel map showing parcels 3303, 3206, & 3207

L. Sawyer

County Tax Bill for 2014 for parcel 3202 owned by Louis P. Taylor

M. Sawyer

County Tax Bill for 2014 for parcel 3303 owned by LCO

N. Sawyer

County Tax Bill for 2015 for parcel 3202 owned by Louis P. Taylor

0. Sawyer County Tax Bill for 2015 for parcel 3303 owned by

LCO

FOR A FULL COPY OF THIS COMPLAINT FORM WITH ALL THE DOCUMENTS LISTED ABOVE, AND SOME ARE NOT PRINTED IN THIS ARTICLE, SUCH AS THE ST. CROIX TRIBAL COURT COMPLAINT DOCUMENT AGAINST CHAIRMAN TAYLOR'S SON, JEFF TAYLOR, EMAIL REQUEST FOR DOCUMENT TO JOEREZLIFE@GMAIL.COM.

IMAGES OF ALL SAWYER COUNTY DOCUMENTATION WILL FOLLOW AT THE BOTTOM OF THIS ARTICLE...

Big Fish Golf Club - Operations & Future Updates

Presented to the Board of Directors

Prepared by: Joe Morey, General Manager Date: April 7, 2025

1. Golf

Operations

With temperatures rising and conditions improving, we are targeting Thursday for course opening, with a possibility of Wednesday if drying conditions allow. There is no longer frost, and with temperatures expected to exceed 60 degrees, we believe this is a safe and exciting time to officially open. I am requesting board approval to move forward with this plan and begin public announcements.

Our grounds crew had previously prepped the course

for an earlier warm-up before

snowfall delayed us. As a result,

the course is currently in a nearly ready state. Preparations included:

-

Removing and cleaning up hazardous trees.

- Clearing downed trees near

fairways and cart paths to enhance playability and aesthetics.

- Equipment

maintenance has been ongoing, but aging equipment remains a concern. I am

requesting approval for new fairway and greens mowers, financed with an option

for early loan payoff at seasons end. This upgrade is critical for both

efficiency and course quality.

2. Marketing

Progress

The addition of Sean Whyte as our Marketing Specialist has been transformative. His work, in conjunction with my marketing background, has greatly accelerated our growth this winter.

-

Website Overhaul: Sean has developed

a new website ready to launch which will exceed the

capabilities of our existing

ForeUp system, allowing

us to eliminate that software

for marketing purposes.

- Marketing Channels: We now

run a robust marketing mix that includes:

- Consistent social media engagement

- Regular email newsletters

- Print and radio advertising

- Enhanced customer service

and food quality standards

- Strategic event planning

Membership & Rounds:

- Rounds of golf are projected to exceed 30,000 this season (compared to 21,000 last year and 27,000 two years ago).

- New members

have shared positive feedback, specifically citing the excitement and

improvements happening at Big Fish.

3. Food

& Beverage Growth

Our food and beverage operations are expanding dramatically.

- New POS

system (installation begins Tuesday, April 8) will streamline inventory

control, integrate with the new website, and allow online ordering.

- On-cart ordering will launch

once new carts arrive.

-

Food point-of-sale stations:

- On the 14th tee box

- Food truck located at the

Tribes Hayward Fame lot

Service Enhancements:

- Two beverage carts will run during peak hours (a major improvement over past years).

-

Current service network includes:

- Two restaurants

- Two bars

- Food truck

- Food stand on 14

- Two beverage carts

- Full delivery in the Hayward

area

- Online and on-cart ordering

-

Remaining work cannot proceed until the outstanding balance of $10,000

is paid.

- Final assembly costs will be

under $3,000.

Conclusion

The team has worked tirelessly to elevate Big Fish in every facet from course prep and staffing to marketing innovation and food service expansion. We are now poised for a record-breaking season. With continued support from the board especially for strategic equipment upgrades and storage infrastructure we can fully realize this momentum.

Checks Haven't Cleared Image Shows Falsehoods

The following image shows the list of checks that hadn't cleared supplied by enterprise bookkeeper Melissa just after misleading the golf board that there was only $6,000 left in the bank account which they relayed to key employees at the course in their effort to discredit me. Note that the Bartingale Mechanical check for $10,152 was not even signed nor authorized at this point and should not have been included in this list. It was only included to inflate the number and discredit. All checks on this list with a checkmark were reported to have cleared at this point.

Now Back to the Chairman's Land Deal

The following are images from the complaint by Adam DeNasha against Chairman Louis Taylor showing the documents from the Register of Deeds of Sawyer County to support Adam's claims.